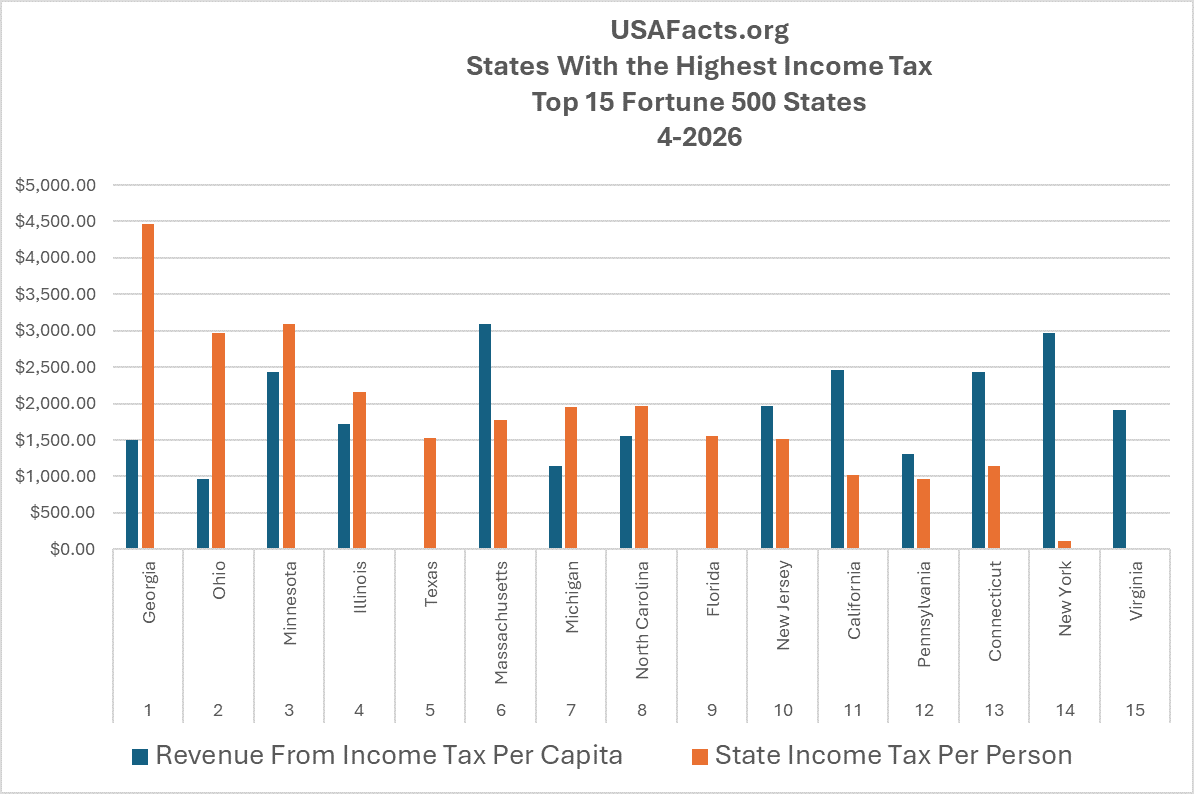

Connecticut Tax Competitiveness: Data Summary and Business Case

It’s tax season and we know you are thinking about what you have to pay to the State and to the Feds. The MetroHartford Alliance reviewed recently released studies that looked at the overall tax burden on individuals, not just the income tax. The two datasets that were analyzed included: USAFacts state income tax data (updated March 2026) and WalletHub's comprehensive Tax Burden by State report (March 31, 2026), which measures each state's total tax burden as a percentage of personal income across property, individual income, and sales/excise categories. Connecticut's overall national ranking is #17 of 50 states with a 9.00% total tax burden. However, there is more to the story when you compare us with our peer states. (i.e., the other Top 15 Fortune 500 states).

Connecticut vs. Top 15 Fortune 500 States — The Business Case

When measured against the 15 states with the highest Fortune 500 headquarters concentrations, Connecticut's tax profile is more competitive than its national ranking suggests. Among this peer group, Connecticut ranks 7th of 15 in total burden — squarely in the middle — but the composition of that burden tells a more favorable story for business attraction.

On individual income tax burden, Connecticut comes in at 2.69%, ranking 5th highest among peers. However, four of the six states that lead Connecticut in this category — New York (4.65%), Massachusetts (3.45%), Minnesota (3.34%), and California (3.03%) — are states that corporations routinely compete against for talent. Connecticut's income tax burden is meaningfully lower than all four, representing a direct, quantifiable take-home pay advantage for relocating executives and professional employees.

The strongest competitive differentiator is Connecticut's sales and excise tax burden of just 2.65%, ranking #44 nationally and second lowest among all 15 Fortune 500 peer states. This matters to both employers and employees: lower consumption taxes compound with income tax savings to produce measurably higher real purchasing power. By contrast, the two "no income tax" states in the peer group — Texas (4.27%) and Florida (3.74%) — offset their zero-income tax with significantly higher sales and excise burdens, narrowing the lifestyle advantage those states often promote.

The net result is a compelling positioning argument: Connecticut offers the talent ecosystem and proximity of the Northeast corridor at a total tax cost below New York, New Jersey, Illinois, California, Minnesota, and Ohio — six of the most active Fortune 500 states in the country. For companies evaluating regional headquarters, insurance and financial services operations, or senior leadership relocations, Connecticut's tax structure represents a substantive cost-of-living advantage that translates directly into compensation competitiveness without requiring higher gross salaries.